The lending industry didn’t intentionally build fragmented systems.

Fragmentation was the cumulative result of solving each new problem with another layer of technology.

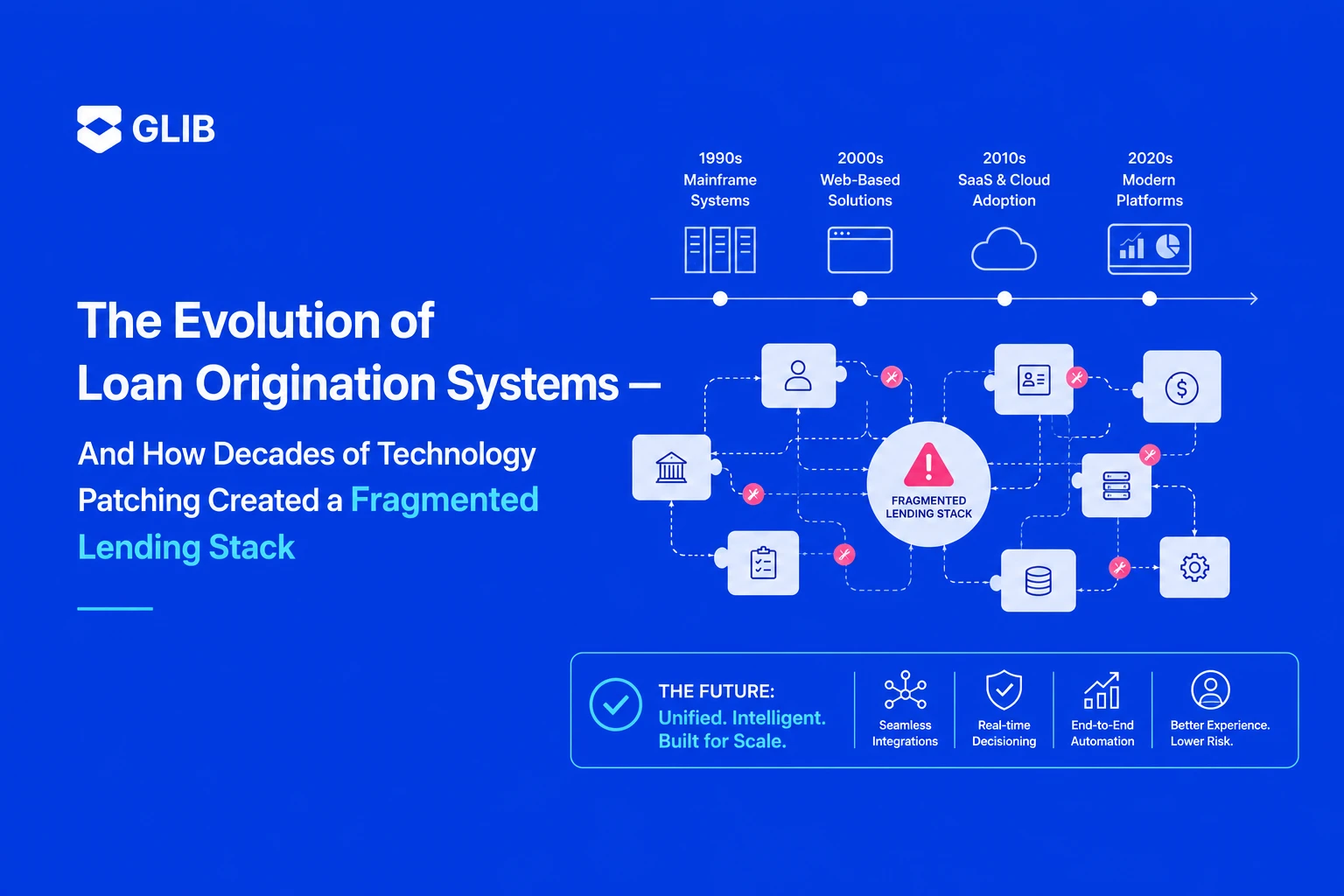

For nearly three decades, Loan Origination Systems (LOS) have remained central to lending operations. Every generation of financial technology innovation promised to modernize lending through:

- Workflow automation

- Digital onboarding

- OCR

- Credit scoring

- APIs

- AI

- Fraud detection

- KYC automation

- Low-code orchestration

- Decision engines

- Generative AI

Individually, each advancement solved an important operational problem.

Collectively, however, they created something few institutions anticipated:

A highly fragmented operational architecture.

Today, many lenders operate environments where:

- Workflows are distributed across multiple systems

- Business logic exists in disconnected layers

- Fraud intelligence is siloed

- Compliance checks are duplicated

- AI tools operate independently

- Customer journeys break across systems

- Operational visibility becomes increasingly difficult

Ironically, the more technology lenders adopted, the more operational complexity they accumulated.

To understand why this happened, it’s important to understand how Loan Origination Systems evolved over time.

Phase 1: The Birth of LOS — Workflow Digitization Era

The earliest Loan Origination Systems emerged primarily to solve a straightforward operational problem:

Replace manual, paper-heavy lending workflows.

At the time, lending operations were highly dependent on:

- Spreadsheets

- Physical documents

- Manual approvals

- Branch coordination

- Paper-based audit trails

The first generation of LOS platforms focused on:

- Application tracking

- Workflow management

- Task routing

- Approval hierarchies

- Operational recordkeeping

This was transformational for the industry.

For the first time, lenders could:

- Standardize operations

- Improve auditability

- Reduce manual delays

- Digitize process flows

However, these systems were fundamentally designed around process coordination—not intelligence.

At that stage, that was sufficient.

Phase 2: The Rise of Rule Engines and Credit Automation

As lending volumes increased, institutions needed greater operational efficiency.

This introduced:

- Automated decision rules

- Credit scoring integrations

- Bureau APIs

- Eligibility logic

- Underwriting automation

LOS platforms began integrating rule engines to automate repetitive decisions.

This created the second major architectural shift:

Workflow systems started absorbing decision logic.

Initially, this improved speed significantly.

However, it also introduced the first signs of structural complexity:

- Business rules embedded inside workflows

- Duplicated logic across products

- Increasingly rigid architectures

- Hardcoded decision dependencies

The system became operationally heavier.

Still, the industry largely viewed this as manageable complexity.

Phase 3: Digital Lending and the API Explosion

The emergence of digital lending dramatically accelerated technology fragmentation.

Customer expectations shifted toward:

- Instant onboarding

- Digital document submission

- Mobile-first experiences

- Real-time approvals

To support this, lenders rapidly integrated:

- eKYC providers

- OCR tools

- Video KYC systems

- e-signature platforms

- Payment gateways

- Account aggregators

- API aggregators

- Fraud detection vendors

This created the best-of-breed integration era.

Every operational challenge was solved by introducing another specialized technology provider.

The architecture evolved from a single operational platform into an interconnected vendor ecosystem.

Initially, this appeared strategically advantageous.

Institutions gained flexibility and innovation speed.

Over time, however, the operational stack became increasingly fragmented.

Phase 4: AI and Point Intelligence Systems

The next wave introduced AI.

Lenders adopted:

- AI-based OCR

- Fraud scoring models

- Alternative data analytics

- Machine learning underwriting

- Conversational AI

- Anomaly detection

- Predictive analytics

Again, each technology addressed a real business need.

However, AI adoption often occurred in silos.

- Fraud teams implemented separate intelligence systems.

- Risk teams adopted independent scoring engines.

- Operations deployed workflow bots.

- Compliance added standalone monitoring tools.

The result?

Intelligence became fragmented across departments.

Organizations unintentionally created:

- Multiple sources of intelligence

- Disconnected AI pipelines

- Inconsistent decision-making

- Fragmented governance

- Overlapping automation layers

Ironically, AI increased operational complexity faster than it reduced it.

The Fundamental Problem: LOS Architecture Was Never Designed for Continuous Intelligence

This is the core issue many institutions are now confronting.

Traditional LOS systems were originally designed for:

- Predefined workflows

- Sequential processing

- Deterministic rules

- Operational coordination

Modern lending environments now require:

- Contextual reasoning

- Real-time adaptation

- Continuous risk evaluation

- Behavioral intelligence

- Dynamic orchestration

- Explainable AI governance

This creates an architectural mismatch.

The problem isn’t that LOS systems failed.

The problem is that the intelligence requirements of lending evolved beyond workflow-centric architectures.

How Technology Patching Created Operational Fragmentation

Over time, lenders continuously patched new capabilities onto existing systems.

Each new challenge introduced another layer:

- Fraud systems

- OCR vendors

- KYC platforms

- Scoring engines

- Workflow tools

- AI copilots

- Compliance monitoring

- Orchestration engines

Very few institutions redesigned the operational architecture itself.

As a result:

The institution became the orchestration layer.

This introduced several structural problems:

- Fragmented decision logic

- Siloed intelligence

- Increasing integration complexity

- Difficult governance

The Industry Is Now Shifting Toward Intelligence Consolidation

Forward-looking institutions are recognizing that the next competitive advantage won’t come from adding more isolated tools.

It will come from consolidating intelligence orchestration.

This is why Agentic Decisioning & Automation Platforms are emerging.

These platforms operate as:

- Intelligence orchestration layers

- Contextual reasoning systems

- Adaptive decisioning infrastructures

- Governance-aware automation platforms

Their purpose is not merely to automate workflows.

Their purpose is to unify:

- Intelligence

- Orchestration

- Compliance

- Automation

- Decision-making

Across fragmented operational environments.

From Systems of Process to Systems of Intelligence

Historically, Loan Origination Systems functioned primarily as systems of process.

Modern lending increasingly requires systems of intelligence.

That means systems capable of:

- Reasoning across fragmented data

- Adapting dynamically

- Orchestrating decisions contextually

- Embedding compliance continuously

- Learning operationally

- Augmenting human judgment

This is not simply better automation.

It is an entirely new operational architecture.

Conclusion

The evolution of Loan Origination Systems mirrors the broader evolution of enterprise technology itself.

Every generation of innovation solved an immediate operational challenge.

But decades of incremental technology patching also created fragmented lending architectures that are increasingly difficult to scale intelligently.

The industry is now entering the next phase:

Moving from fragmented automation ecosystems toward unified intelligence infrastructures.

The future of lending will not belong to institutions with the most tools.

It will belong to institutions capable of orchestrating intelligence, automation, compliance, and decision-making as a single adaptive operational system.

See Agentic Decisioning & Automation in Action

Ready to modernize your lending operations?

Learn how GLIB helps financial institutions unify AI, workflows, and decision intelligence into a single operational platform.