Artificial Intelligence has become a central pillar of modern lending.

Financial institutions are using AI to automate income verification, analyze bank statements, assess creditworthiness, and accelerate loan approvals at unprecedented scale.

The benefits are undeniable:

- Faster decisions

- Lower operating costs

- Improved customer experiences

As a result, AI has become a strategic priority for banks, NBFCs, and fintech lenders worldwide.

Yet as AI adoption grows, a new challenge is moving to the forefront:

Can institutions trust the decisions their AI systems make?

Across the lending industry, the conversation is shifting from automation to accountability.

Financial institutions are increasingly recognizing that speed alone is not enough. AI-driven underwriting must also be explainable, auditable, and fair.

The Hidden Risk Inside Historical Data

Most underwriting models learn from historical lending data.

The challenge is that historical data reflects past decisions, economic conditions, and human judgment.

While it contains valuable signals about repayment behavior, it can also carry unintended biases.

Several financial institutions have publicly acknowledged that early AI models sometimes reproduced patterns that disproportionately affected specific customer segments or geographic regions.

These outcomes were not intentional, but they highlighted an important reality:

AI can only be as fair as the data and governance frameworks behind it.

As a result, lenders are investing heavily in:

- Model governance

- Fairness audits

- Explainability frameworks

The goal is to ensure that automated decisions remain objective, consistent, and compliant.

Why Explainability Matters More Than Ever

For decades, underwriting decisions followed a relatively straightforward path.

Credit teams could review financial information, understand the rationale behind a decision, and explain it when required.

Many AI models introduce a level of complexity that makes this process more difficult.

If a customer is denied credit, risk teams, auditors, and regulators increasingly expect institutions to answer a simple question:

Why?

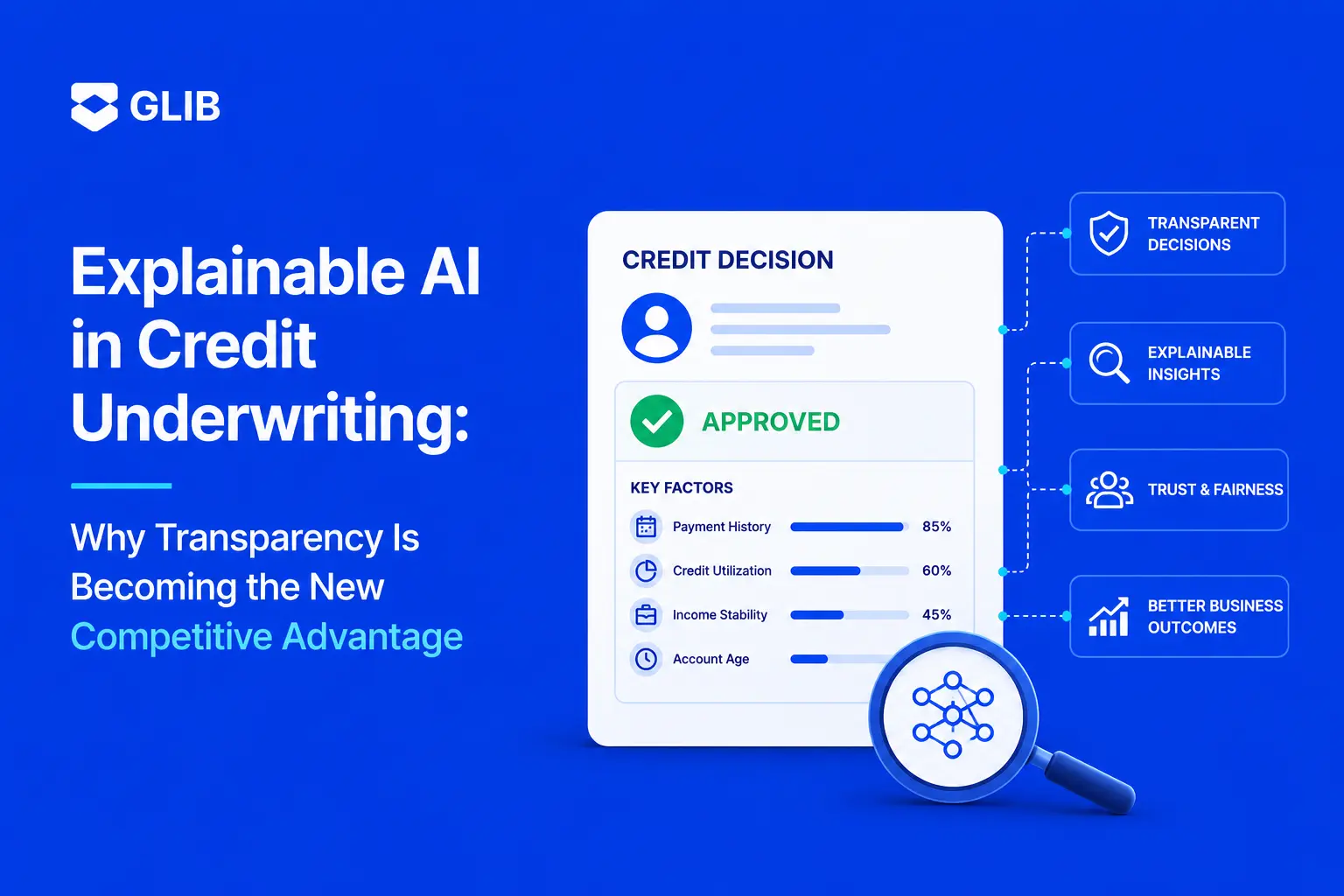

This is where explainable AI becomes critical.

Modern explainability frameworks help lenders understand which factors influenced a credit decision, including:

- Income stability

- Repayment history

- Banking behavior

- Debt obligations

- Cash flow patterns

The objective goes beyond regulatory compliance.

Explainability builds trust across the entire lending ecosystem.

Benefits of Explainable AI

For Customers

- More transparent credit decisions

- Better understanding of approval and rejection outcomes

For Risk Teams

- Greater confidence in model outputs

- Improved decision validation

For Compliance Teams

- Easier assessment of fairness and consistency

- Better auditability

For Regulators

- Improved visibility into governance controls

- Stronger confidence in risk management frameworks

Explainability transforms AI from a black box into a decision-support system that organizations can confidently deploy at scale.

The Industry’s Shift Toward Human-Guided AI

An important trend is emerging across banks, fintechs, and lending institutions.

Rather than replacing human underwriters entirely, organizations are increasingly using AI to augment decision-making.

AI is being deployed to:

- Collect and validate financial data

- Extract information from bank statements and financial documents

- Identify risk signals and anomalies

- Generate recommendations for underwriters

- Prioritize applications based on risk profiles

Human experts remain responsible for:

- Reviewing complex cases

- Validating exceptions

- Making final lending decisions when necessary

This hybrid approach combines the efficiency of automation with the judgment and accountability of experienced credit professionals.

Fighting Bias Through Governance

Responsible AI requires more than advanced algorithms.

Leading institutions are implementing governance mechanisms designed to reduce bias and improve reliability.

Fairness Audits

Regular reviews of model outcomes across different customer groups help identify unintended bias.

Data Quality Controls

Organizations ensure that models rely on verified financial information rather than incomplete or unreliable inputs.

Model Monitoring

Continuous performance tracking helps identify:

- Model drift

- Emerging risk patterns

- Changes in borrower behavior

Human Oversight

Review checkpoints are introduced for:

- Edge cases

- High-risk applications

- Exception-based lending decisions

Together, these controls help organizations maintain consistency while reducing the risk of unfair or inaccurate outcomes.

What This Means for the Future of Underwriting

The next phase of AI adoption in financial services will not be defined by who automates the fastest.

It will be defined by who can automate responsibly.

As regulators increase scrutiny and customers demand greater transparency, explainability will become a core requirement rather than a competitive differentiator.

The institutions that succeed will be those that can clearly demonstrate:

- How decisions are made

- Which data sources are used

- Why specific outcomes occur

- What controls exist to prevent bias and errors

In short, the future belongs to AI systems that are not only intelligent, but accountable.

Where GLIB Fits In

At GLIB, we see this evolution happening across lending operations every day.

Whether it’s:

- Bank statement analysis

- Income verification

- Financial statement spreading

- Underwriting workflows

Financial institutions increasingly want more than document automation.

They want systems that create transparency throughout the decision-making process.

The next generation of lending platforms must help organizations:

- Understand the data behind every recommendation

- Validate financial information with confidence

- Support risk teams with auditable decision intelligence

Because in modern underwriting, trust is becoming just as important as automation.

Conclusion

AI is reshaping credit underwriting, but the industry’s priorities are evolving.

The focus is no longer simply on processing more applications faster.

It is on building underwriting systems that are:

- Transparent

- Explainable

- Fair

For lenders operating in an increasingly regulated and competitive environment, explainable AI is quickly becoming a strategic necessity.

The question is no longer whether AI should be part of underwriting.

The question is whether institutions can fully trust the decisions their AI makes.

Key Takeaways

- AI adoption in lending is shifting from automation to accountability.

- Historical data can introduce bias if governance is not properly implemented.

- Explainable AI improves transparency, fairness, and trust.

- Human-guided AI is emerging as the preferred underwriting model.

- Governance frameworks are becoming essential for responsible lending.

- The future of underwriting belongs to AI systems that are both intelligent and accountable.

👉 Looking to build transparent, explainable underwriting workflows with AI?